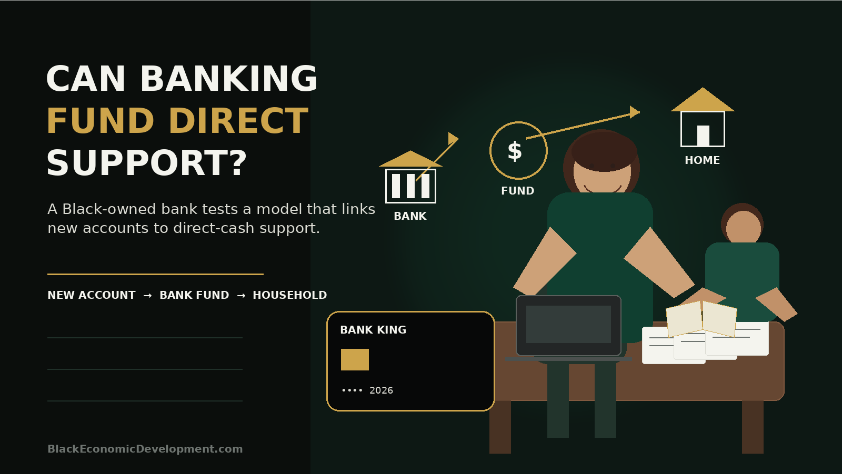

Redemption Bank is using Juneteenth to introduce more than a branded debit card.

The Black-owned bank launched the Bank King Card on June 19, 2026, with a promise to make fixed donations based on the number of new accounts opened.

Those funds will flow through the Redemption Foundation to nonprofits that provide unrestricted cash support to single mothers, including women living in government-subsidized housing.

The customer does not pay an added donation or need to spend a certain amount.

The bank says its board will determine the fixed contribution per new account annually, and the donation will not be tied to card-purchase volume.

That distinction is important.

This is not a traditional rewards card that returns a percentage of spending to the cardholder. It is also not a checkout-roundup program funded directly by consumers.

Instead, Redemption Bank is proposing to connect its own customer-acquisition growth to direct economic support for families.

The idea raises a larger question for Black banking: Can representation inside the financial system be converted into a recurring mechanism for redistributing value?

What the Bank King Card actually does

The Bank King Card is currently available as a debit product that can be used wherever Mastercard is accepted. Redemption Bank says a credit-card version will follow, with interest capped at 12%.

For each qualifying new account, Redemption Bank intends to contribute a fixed amount to the Redemption Foundation. Nonprofits that deliver direct-cash programs can then apply for foundation grants.

One of the foundation’s initial partners is the Georgia Resilience and Opportunity Fund, or GRO Fund. Its In Her Hands initiative provides unrestricted cash to women for expenses that can include housing, childcare, transportation, education and healthcare.

The structure creates a chain:

New customer ? bank donation ? foundation grant ? nonprofit program ? direct household cash

That is the model’s central economic promise.

But several numbers have not yet been made public.

Redemption Bank has not disclosed the donation amount attached to each new account, an annual funding target or the number of mothers expected to receive support. The amount will be set by the bank’s board each year.

Without those figures, the launch can be evaluated as a credible structure. But not yet as a proven economic intervention.

The economics depend on customer growth

The program’s funding is tied to account openings, not ongoing card spending.

That gives the bank a straightforward incentive: more customers should mean more donations.

It also means the social impact could slow if account growth slows.

Consider the basic formula:

New accounts × fixed contribution = annual program funding

A $10 contribution attached to 10,000 new accounts would produce $100,000. A $50 contribution would produce $500,000.

Those are illustrations, not disclosed Bank King Card terms. The actual impact cannot be calculated until the bank publishes its contribution per account and account-opening results.

That transparency will matter because the product’s social value is not determined by the card’s symbolism. It is determined by how much money reaches households.

The bank should eventually report:

- New Bank King Card accounts opened

- Donation amount per account

- Total foundation contributions

- Administrative expenses

- Nonprofit grant recipients

- Number of mothers served

- Average cash support per household

- Measurable household outcomes

Those figures would allow consumers to determine whether the model is primarily a marketing strategy, a modest philanthropic program or a scalable financial intervention.

Why unrestricted cash matters

Direct-cash programs differ from traditional assistance programs because recipients generally have greater discretion over how to use the money.

The AP cited the Ohio Mother’s Trust, which provided $500 per month for one year to 32 single mothers. It also highlighted Michigan’s Rx Kids program, which provides eligible mothers with a $1,500 prenatal payment followed by monthly payments during infancy. Recipients described using the funds for rent, bills, diapers, food and other immediate needs.

The economic logic is simple: families experiencing financial instability often face several pressures at once.

A transportation problem can affect work. A childcare gap can interrupt income. An overdue utility bill can become a late fee, reconnection fee or debt. A small amount of flexible cash can prevent one expense from triggering a larger financial setback.

That does not mean a limited cash program can solve structural poverty.

Direct payments do not replace affordable housing, accessible childcare, higher wages, healthcare coverage or equitable access to credit.

But they can give households flexibility that tightly restricted benefit programs often do not.

From Black ownership to Black economic function

Redemption Bank became the first Black-owned bank headquartered in the Mountain West after Redemption Holding Company completed its acquisition of a Utah bank in June 2025.

The institution had approximately $65 million in assets at the time and planned to focus heavily on commercial and small-business lending.

The acquisition itself was historically significant. A Black-led investment group acquired a non-minority-owned bank and converted it into a Black-owned institution. A different path from starting a new bank from scratch.

But ownership is only the first layer.

The stronger economic question is what the institution does with the deposits, lending authority, customer relationships and financial infrastructure it controls.

A Black-owned bank can create value through several channels:

- Extending credit to underserved businesses

- Paying employees and vendors

- financing housing and commercial property

- retaining deposits within a Black-controlled institution

- designing lower-cost financial products

- directing part of its revenue toward community investment

The Bank King Card adds another possible function: using account growth to finance direct household support.

That moves the conversation from representation toward institutional behavior.

BlackEconomicDevelopment.com’s editorial framework asks not only who owns an institution, but who controls its capital, who captures the upside and who carries the risk.

The planned 12% credit card could be the larger consumer test

Redemption Bank says a Bank King credit card will follow with interest capped at 12%.

That feature could have a more direct effect on cardholders than the debit-card donation model.

Lower interest reduces the cost of carrying a balance. The actual savings would depend on the borrower’s balance, repayment behavior and the interest rate they would otherwise receive.

The important details have not yet been published.

Consumers will need to know:

- Whether the 12% cap is fixed or variable

- The annual fee, if any

- Eligibility and underwriting standards

- Late-payment and penalty terms

- Balance-transfer conditions

- Credit limits

- Whether the foundation donation also applies to credit accounts

The interest-rate cap is promising, but a low advertised rate should be evaluated alongside all fees and access requirements.

Redemption Bank’s current deposit-account disclosures show free checking with no monthly service charge or minimum balance, but they also list overdraft interest and several transaction-related fees.

Those existing terms reinforce the need to judge the Bank King Card from its complete disclosures rather than its headline features alone.

Who benefits—and who carries the risk?

Redemption Bank can benefit by attracting customers who want their banking activity aligned with a social mission.

The foundation and its nonprofit partners can receive a recurring funding source.

Single mothers can gain flexible cash that may help cover housing, transportation, childcare, education or emergency expenses.

Customers may gain a values-based banking option and, eventually, access to a credit product with a lower interest ceiling.

But the risks are distributed differently.

The bank carries the cost of the donations and the reputational risk if the impact remains too small or poorly documented.

Nonprofits carry the administrative burden of identifying recipients, delivering payments and reporting results.

Families carry the greatest economic risk if the program is marketed as transformational but produces limited, inconsistent or temporary support.

That is why the size, regularity and governance of the funding matter.

Can the model scale?

The model is most likely to scale if it accomplishes three things at the same time:

First, the card must be competitive as a banking product. Customers are unlikely to stay solely because of the mission if the digital experience, customer service, ATM access, fees or fraud protection are weak.

Second, the donation must be large enough to create meaningful funding. A high number of accounts paired with a very small contribution could generate attention without substantial household impact.

Third, Redemption Bank must publish results. A transparent annual impact report could show whether account growth is producing meaningful transfers to mothers and children.

The bank could also strengthen the model by establishing a minimum annual contribution, obtaining matching commitments from institutional partners or allowing customers to see the cumulative impact associated with the program.

Those additions could turn the card from a one-time Juneteenth announcement into a recurring piece of financial infrastructure.

Juneteenth symbolism versus measurable economics

The launch date is deliberate.

The Bank King Card debuted on Juneteenth and on the first anniversary of Redemption Holding Company’s acquisition of the institution. Bernice A. King, the daughter of Martin Luther King Jr., is a co-founder and senior vice president of the bank.

That positioning gives the product cultural and historical meaning.

But symbolism is not the same as economic impact.

The product will matter most if it can demonstrate that everyday banking activity helped mothers avoid debt, maintain housing, afford childcare, stay employed or build greater financial stability.

The strongest version of this model would show that a Black-owned institution can compete for customers while deliberately designing a portion of its growth to reach households under economic pressure.

That is a more demanding standard than representation.

It is also a more meaningful one.

“The product’s social value will not be determined by its Juneteenth symbolism. It will be determined by how much money reaches households—and what that money allows families to do.”

Economic interpretation

Redemption Bank is attempting to convert customer acquisition into a social-finance mechanism.

Instead of asking customers to make an added donation, the bank plans to fund contributions from the economic value associated with new accounts.

The model could demonstrate how a Black-owned financial institution uses ownership differently. Not only by expanding representation, but by embedding community investment into a consumer product.

Its credibility will depend on disclosed donation amounts, transparent administration and measurable household outcomes.

Where the money moves

Money moves from Redemption Bank to the Redemption Foundation. Then through nonprofit grants into direct-cash programs serving single mothers.

The bank also gains deposits and customer relationships from new accounts, which can support lending and other revenue-generating activity.

Who owns and controls the system

Redemption Bank controls the product, customer relationship and annual contribution decision.

Its board determines the donation amount.

The Redemption Foundation controls grantmaking, while partner nonprofits administer direct-cash programs.

Recipients control the use of unrestricted household payments.

Who captures the upside

Redemption Bank gains deposits, visibility and customer growth.

Nonprofits gain funding.

Mothers gain flexible cash.

Customers gain a banking product connected to a stated social purpose and may later gain access to credit capped at 12% interest.

Who carries the risk

Families carry the risk that funding is too small or inconsistent.

Customers carry product-level risks related to fees, service quality and future credit terms.

The bank carries financial and reputational risk.

Nonprofits carry the delivery and accountability burden.

Why it matters

Black ownership in banking matters because banks allocate credit, hold deposits and shape the cost of financial access.

The Bank King Card asks whether that ownership can also support an intentional redistribution mechanism.

The answer will depend less on branding than on scale, disclosures and outcomes.

Latest posts by normbond (see all)

- FIFA Wants to Turn the World Cup Into a $20 Billion Company. Who Owns Global Football After That? - July 29, 2026

- Cape Town Approved a 170-Megawatt Data-Center Project. The Community Still Does Not Know the Full Resource Cost. - July 29, 2026

- LeBron Took an $8 Million Deal. The 76ers May Capture the Bigger Economic Win. - July 24, 2026