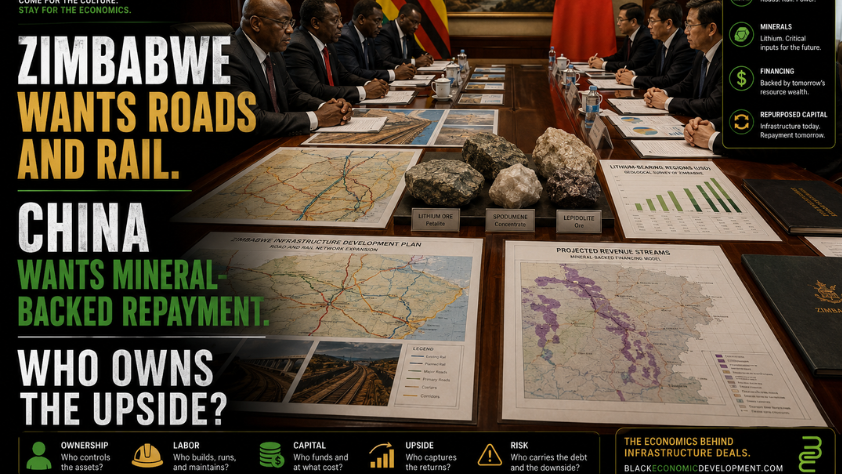

Zimbabwe needs roads and railways capable of moving people, goods and minerals across the country.

China has the construction capacity and financing channels to help build them.

The question is what Zimbabwe may have to pledge in return.

Finance Minister Mthuli Ncube said the government has begun discussions with China Railway about financing transport projects through future revenue from natural resources. Under the arrangement being considered, loans for specific road and railway projects would be repaid using mineral-linked income.

Zimbabwe is not simply shopping for a construction contractor.

It is considering converting future mineral earnings into financing today.

That could accelerate infrastructure development without requiring the government to produce the full cost upfront.

It could also commit income from lithium and other resources before Zimbabwe has secured stronger domestic processing capacity, pricing power and public oversight.

That is the economics behind it.

Zimbabwe’s infrastructure gap is real

Zimbabwe’s transport system has suffered from years of underinvestment, economic instability and limited access to international finance.

The African Development Bank estimates that the country needs about $34 billion to modernize its transport and logistics networks.

Weak roads and railways raise the cost of nearly every economic activity.

Farmers pay more to move crops.

Manufacturers face higher logistics expenses.

Mining companies struggle to transport equipment and exports efficiently.

Consumers ultimately absorb part of those costs through higher prices and limited product availability.

Better infrastructure could improve trade, lower transportation expenses and make Zimbabwe more competitive within regional markets.

The need is not in dispute.

The financing structure is where the economic questions begin.

How mineral-backed financing works

Resource-backed financing allows a government to borrow for infrastructure and repay the debt using future earnings from oil, minerals or other natural resources.

Instead of relying only on tax revenue or traditional sovereign borrowing, the country connects repayment to the value generated by a specific asset base.

For Zimbabwe, that could mean using future income from lithium or other minerals to support loans for road and rail construction.

The structure can appeal to governments that have large infrastructure needs but limited access to conventional credit markets.

Zimbabwe has spent years trying to address external debt arrears and rebuild access to international capital. In 2024, the country was seeking to restructure approximately $12.7 billion in external debt.

Mineral-backed financing may provide another route to capital.

But it can also move part of the country’s future resource income outside the normal budget process.

The key issue is not simply whether minerals support infrastructure.

It is who controls the terms, who receives the contracts, how repayment is calculated and what happens if mineral prices fall.

Lithium gives the proposal more weight

Zimbabwe has become Africa’s leading lithium producer and an increasingly important supplier to China’s battery-material supply chain.

In 2025, the country exported 1.128 million metric tons of spodumene concentrate, with most of that material shipped to China for further processing.

Chinese battery-material companies have invested more than $1.4 billion in Zimbabwean lithium assets since 2021, according to Reuters reporting and data cited by Zimbabwe’s Minerals Marketing Corporation.

That investment has helped expand production.

It has also increased Chinese influence across mine ownership, processing decisions and export routes.

Major Chinese-linked companies operating in the sector include Zhejiang Huayou Cobalt, Sinomine, Chengxin Lithium Group and Yahua Group.

Zimbabwe controls the minerals beneath its soil through the authority of the state.

But control over extraction capital, processing technology, purchasing relationships and export markets is more distributed—and increasingly connected to Chinese firms.

Adding infrastructure finance to that relationship could deepen the connection between Zimbabwe’s mineral sector and Chinese capital.

Who captures the immediate upside?

A mineral-backed infrastructure agreement could create several winners.

Chinese contractors could gain large road and railway construction projects.

Chinese-linked mining companies could benefit from better transport connections between mines, processing plants and export corridors.

Logistics companies could move more freight at lower cost.

Zimbabwean mining and agricultural exporters could gain more reliable routes to regional ports and markets.

The government could obtain infrastructure sooner than it might through normal budget financing.

Communities could benefit from improved mobility if projects connect towns, farms, businesses, schools and hospitals—not only mining zones.

But those gains depend heavily on which roads and railways are selected.

Infrastructure that connects communities and domestic industries creates a wider development benefit.

Infrastructure designed primarily to move ore from foreign-owned mines to export routes may improve extraction without building broader industrial capacity.

The road itself does not answer the ownership question.

Its route, users, toll structure, procurement terms and connection to domestic industry do.

Who carries the risk?

Zimbabwean taxpayers and future governments may carry the long-term repayment risk.

If projected mineral revenue falls short, the government may have to redirect public resources, extend the agreement or renegotiate the debt.

Mineral prices are volatile.

Zimbabwe’s spodumene export volume increased in 2025, but revenue remained almost flat because weaker lithium prices offset the higher output. Export revenue was about $513.8 million, slightly below the previous year, despite an 11% increase in volume.

That is an important warning.

More minerals do not automatically produce more revenue.

If repayment commitments are based on optimistic commodity prices, a market downturn could leave Zimbabwe delivering more resources—or sacrificing more public income—to meet the same debt obligation.

Communities near mining areas may also carry environmental and social costs through land disruption, water pressure, pollution or displacement.

Future governments could inherit agreements they did not negotiate but are still required to honor.

The contractor gets paid during construction.

The country carries the repayment obligation for years.

The processing question may matter most

Zimbabwe has already recognized that exporting low-value mineral concentrates leaves too much of the economic upside elsewhere.

The government plans to prohibit exports of lithium concentrate beginning in 2027 as part of an effort to encourage more domestic processing and value addition.

That policy could help Zimbabwe capture more value from refining, chemical conversion, technical employment and industrial development.

But miners have asked for more time to construct the required processing facilities, highlighting the capital and technical challenges involved.

This creates a tension.

Zimbabwe may use future mineral revenue to finance infrastructure.

At the same time, it is still trying to build the domestic processing capacity needed to increase the value of those minerals.

If mineral revenue is committed before that transition occurs, the country may effectively pledge earnings based on a lower-value position in the supply chain.

The strongest financing deal would not merely build routes for moving minerals out.

It would help Zimbabwe move up the value chain.

Roads for extraction or infrastructure for development?

Infrastructure is not economically neutral.

A railway from a mine to a border post serves a different development function from a network connecting mines to local processing plants, industrial parks and domestic manufacturers.

Both can increase exports.

Only one may create a broader industrial ecosystem.

Zimbabwe should therefore evaluate the proposed financing around more than construction cost and completion speed.

The government should ask:

- Will Zimbabwean firms receive meaningful procurement opportunities?

- Will local workers gain technical training?

- Will the rail system serve domestic passengers and producers as well as mining companies?

- Will logistics fees remain inside Zimbabwe?

- Will infrastructure connect mineral extraction to domestic processing?

- Will the public be able to examine the repayment formula?

These questions determine whether the country is financing national development or mainly improving the efficiency of extraction.

China is not the only actor with interests

The story should not be reduced to a simple narrative of China taking resources from an African country.

Zimbabwe is actively seeking capital and infrastructure.

Chinese firms are responding to real economic demand and accepting commercial and political risks that many Western lenders and contractors have avoided.

China also has a strategic interest in securing access to critical minerals needed for batteries, electric vehicles and energy storage.

Zimbabwe has an interest in turning mineral wealth into roads, rail, industry and public revenue.

The two sides can both benefit.

But equal benefit does not happen automatically.

It depends on negotiating capacity, contract transparency, local-content requirements, pricing formulas and Zimbabwe’s ability to retain control over high-value parts of the supply chain.

The economic question is not whether Zimbabwe should work with China.

It is whether Zimbabwe can negotiate from the position of a mineral owner rather than a distressed borrower.

Why this matters to Black communities and the diaspora

This is one of the central African development questions.

The continent possesses many of the resources required for the global energy transition.

But ownership of minerals does not guarantee control over the industries built around them.

The largest financial gains often occur after extraction—in processing, manufacturing, logistics, technology, financing and distribution.

If African governments pledge future mineral income while foreign firms control extraction, processing and infrastructure delivery, resource ownership can become thinner than it appears.

The state may technically own the minerals.

Foreign companies may control the capital, equipment, purchasing contracts, transport systems and access to global markets.

That is why infrastructure financing must be evaluated as an ownership issue.

A road can be a public asset.

It can also become part of a privately controlled extraction chain.

A railway can support national industrialization.

It can also move raw or semi-processed materials abroad faster.

What Zimbabwe should protect

Mineral-backed financing is not automatically a bad deal.

It can work when projects have a clear economic return, repayment terms are transparent and the infrastructure supports multiple sectors.

But Zimbabwe should protect several things before committing future revenue.

The first is pricing transparency.

The public should understand how mineral revenue will be valued and how much must be committed under different commodity-price scenarios.

The second is processing control.

Infrastructure should support domestic refining and industrial development, not only raw-material exports.

The third is contract visibility.

Parliament, auditors and the public should be able to examine the debt amount, interest cost, repayment period, collateral structure and dispute terms.

The fourth is local economic participation.

Zimbabwean contractors, workers and suppliers should capture a meaningful share of the project spending.

The fifth is public access.

Roads and railways financed through national resource wealth should serve the wider economy, not only foreign-backed mining operations.

The ownership question

Zimbabwe owns the minerals.

But ownership of the resource is only the first layer.

- Who controls the mine?

- Who processes the lithium?

- Who sets the purchase price?

- Who builds and operates the railway?

- Who collects logistics fees?

- Who owns the technology?

- Who receives the contracts?

- Who carries the debt if mineral prices fall?

Those questions determine where the wealth moves.

If the infrastructure increases domestic processing, improves regional trade and creates long-term public assets, mineral-backed financing could turn underground wealth into productive capacity.

If the deal mainly accelerates extraction while assigning future revenue to repayment, Zimbabwe may exchange tomorrow’s mineral income for infrastructure that strengthens someone else’s supply chain.

Infrastructure should build sovereignty

Zimbabwe’s financing challenge is real.

The country cannot industrialize with deteriorating roads, slow rail service and expensive logistics.

But infrastructure is not only about concrete and steel.

It is about economic control.

The strongest agreement would use mineral wealth to build assets that remain productive after the loan is repaid.

It would connect mines to Zimbabwean processing plants.

It would create jobs beyond extraction.

It would give domestic companies access to transport and procurement opportunities.

It would preserve public oversight of repayment obligations.

And it would ensure that Zimbabwe’s lithium supports more than the movement of minerals.

The country should not have to choose between keeping resources underground and trading away future income.

The better goal is to use those resources to build infrastructure, industrial capacity and bargaining power at the same time.

Because the real measure of the agreement will not be how many kilometers of road or railway China builds.

It will be how much economic control Zimbabwe still holds when the debt comes due.

Economic implication

Zimbabwe is considering converting future mineral earnings into present-day infrastructure financing.

That could reduce the country’s transport deficit and support exports. But it may also lock in claims on future lithium and mineral revenue before Zimbabwe has secured stronger domestic processing capacity and more control over the value chain.

Why it matters

Africa’s mineral wealth can finance development, but the structure of financing determines who benefits.

If roads and railways primarily improve extraction and exports, foreign contractors, miners and overseas processors may capture much of the upside.

If the infrastructure supports domestic processing, local procurement and regional trade, mineral wealth can help build sovereign industrial capacity.

Ownership question

Will Zimbabwe retain enough control over lithium processing, transport revenue and export value—or turn future mineral earnings into pre-sold collateral?