The regulator says no public offering has been filed or approved, raising a larger question about whether ordinary investors will receive safe, transparent access to one of Africa’s most important industrial assets.

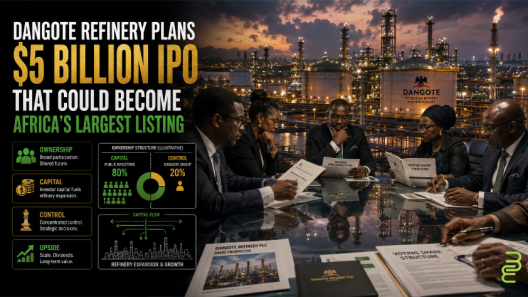

Nigeria’s Securities and Exchange Commission has ordered an immediate halt to unauthorized marketing connected to a purported initial public offering by Dangote Petroleum Refinery & Petrochemicals.

The SEC said no application to register an IPO or public offering of refinery shares had been filed with or approved by the commission.

The regulator said advertisements, digital banners, social-media posts and investment solicitations were already circulating. Some registered capital-market operators were allegedly seeking advance subscriptions tied to the proposed offering.

The SEC directed stockbrokers, digital-platform promoters and other market operators to stop publishing or distributing promotional material related to the acquisition of refinery shares.

It also ordered unauthorized materials removed within 24 hours, told operators to stop accepting deposits or expressions of interest and required any money already collected to be refunded within 24 hours.

That is the immediate regulatory story.

The economics behind it is about who controls investor access, who captures the value created by public demand and who carries the risk when money starts moving before formal disclosure exists.

The Refinery Is Real. The Public Offer Is Not Approved.

The Dangote refinery is a real operating industrial asset with significant economic importance.

Owned by billionaire Aliko Dangote, the refinery began production in 2024 and has the capacity to process 650,000 barrels of crude oil per day. It produces diesel, aviation fuel, naphtha and petrol and has reduced Nigeria’s reliance on imported refined petroleum products.

Plans for a future public listing have attracted widespread attention.

But a company’s intention to list shares is not the same as an approved public offering.

The SEC said the current solicitations included requests for investors to create accounts, pre-fund those accounts or secure supposed guaranteed allocations.

The regulator classified those activities as unauthorized and warned they could mislead investors, distort market expectations and create information asymmetry.

Dangote Petroleum Refinery has also said it did not authorize the recent IPO-related marketing. The company said any potential public offering would be communicated through formal regulatory disclosures.

That distinction matters.

A legitimate company name does not automatically make every offer connected to that name legitimate.

A proposed IPO is not an approved IPO.

And interest in buying shares is not a reason to send money before investors can review formal terms.

Investor Demand Is a Financial Asset

Public enthusiasm has economic value.

When thousands of investors want access to a major company, that demand can help support a higher valuation, attract institutional capital and make it easier for existing owners to sell shares.

Brokers, advisers and digital investment platforms can also earn fees by connecting investors to an offering.

That creates an incentive to get in front of investor demand early.

But there is a major difference between educating potential investors about a future opportunity and collecting money for an offering that has not been approved.

When marketers ask people to pre-fund accounts or reserve allocations before a prospectus is available, they are attempting to control demand before investors receive the information needed to make an informed decision.

The money begins moving before the disclosures do.

That places the investor at a disadvantage.

Who Controls the Asset, Access and Capital?

This story involves several layers of ownership and control.

Dangote owns and controls the refinery.

The company and its existing owners will determine how much equity might eventually be offered, subject to regulatory approval.

Nigeria’s SEC controls access to the regulated public market.

The commission determines whether an offering has met the legal and disclosure requirements necessary to solicit money from the public.

Brokers and digital platforms influence access.

They can shape how an offering is presented, which investors hear about it and where people are directed to open accounts or transfer funds.

Retail investors provide the capital.

But they often possess the least information and carry the greatest risk when an opportunity is promoted prematurely.

That imbalance is why formal approval, disclosure and investor-protection rules matter.

Who Could Capture the Upside?

A properly structured Dangote refinery IPO could create several potential beneficiaries.

- The refinery could raise capital for expansion, operations, logistics or other corporate needs.

- Existing owners could convert part of a privately held asset into publicly traded value.

- Authorized banks, brokers, advisers and other financial intermediaries could earn underwriting and transaction fees.

- Institutional and retail investors could gain exposure to the refinery’s future earnings and growth.

The company has already been seeking about $1 billion through a separate private placement, according to Reuters. The placement reportedly valued the refinery at approximately $39.1 billion and required a minimum subscription of $350,000, placing that opportunity beyond the reach of most ordinary investors.

A future public offering could potentially widen participation.

But whether it produces meaningful public ownership will depend on the final valuation, share allocation, voting rights and percentage of the company made available.

A listing can provide access without transferring meaningful control.

Retail Investors Carry the Immediate Risk

Before an offering is approved, retail investors carry several forms of risk.

They may encounter false allocation promises, misleading advertising or pressure to transfer money before they can review audited financial information and an approved prospectus.

They may not know the final share price, the size of the offering, how shares will be allocated or whether the transaction will proceed.

Even when funds are returned, investors may face delays, lost opportunities and uncertainty.

The operator promoting the investment may have more information, more resources and greater legal protection.

The individual investor may be risking savings accumulated over years.

That is not equal exposure.

The SEC’s intervention is therefore not simply about paperwork. It is about preventing public appetite for ownership from being converted into unprotected liquidity.

Pension Capital Raises the Stakes

The proposed listing may also involve more than individual investors.

In May 2026, Nigeria’s National Pension Commission granted pension fund administrators a special waiver allowing them to invest in the planned Dangote refinery IPO.

The waiver suspended some standard eligibility requirements, including an established profitability and dividend-payment record.

PenCom described the decision as exceptional and tied it to the refinery’s strategic importance and the track record of its parent company. Pension managers must still follow their internal risk controls and fiduciary duties.

That means workers’ retirement savings could eventually be exposed to the refinery’s performance.

The potential benefit is that Nigerian pension capital could participate in a major domestic industrial asset.

The risk is that strategic importance can be confused with guaranteed investment performance.

A company can be important to the national economy and still be overvalued, highly leveraged or exposed to operating and market risks.

Regulatory approval does not eliminate those risks.

It ensures investors receive formal information with which to evaluate them.

Investor Protection Is Not Anti-Ownership

The SEC’s action should not be interpreted as opposition to ordinary Nigerians owning shares in the refinery.

Investor protection is part of the infrastructure that makes broad ownership possible.

Formal rules create accountability around marketing, disclosure, pricing, custody and the handling of investor funds.

They help separate a legitimate public offering from a campaign built primarily on a recognizable corporate name and the fear of missing out.

The goal should not be to keep retail investors away from important African assets.

The goal should be to ensure that they are not treated as unsecured sources of capital before the terms of ownership are known.

Why This Matters to African and Diaspora Investors

Interest in African investment opportunities is growing across the continent and throughout the diaspora.

That interest can support industrial development, infrastructure, entrepreneurship and long-term wealth creation.

But it also creates an audience for promoters who understand that many people want to participate in Africa’s growth story.

The Dangote name carries credibility.

That does not mean every person or platform claiming to offer early access has authorization to do so.

The legitimacy of the asset does not automatically establish the legitimacy of the solicitation.

Before transferring money, investors should verify the offering through the regulator, confirm that the broker or platform is authorized and review the approved prospectus when one becomes available.

African ownership should expand.

But it should expand through transparent markets that give investors enforceable rights and credible information.

The Ownership Question

The central issue is not simply whether the Dangote refinery will eventually go public.

It is what kind of ownership opportunity the public offering will create.

- Will ordinary investors receive fair access to the same information available to institutions?

- Will the shares be priced at a level that reflects both the refinery’s potential and its risks?

- Will enough equity be made available to create meaningful public participation?

- Will Nigerian households and pension contributors capture part of the refinery’s long-term upside?

- Or will retail enthusiasm primarily provide demand, liquidity and favorable pricing for existing owners?

Those questions cannot be answered until formal offering documents are released.

That is exactly why premature marketing matters.

From Public Interest to Public Ownership

The Dangote refinery represents something many African investors want: the opportunity to own part of a major industrial asset built on the continent.

That demand should not be dismissed.

It should be protected.

A credible IPO could connect household savings and long-term institutional capital to African industry.

An opaque or prematurely marketed offer could turn that same desire into fraud exposure, misinformation and financial loss.

Nigeria’s SEC is drawing a necessary line between public interest in ownership and an actual regulated opportunity to invest.

Because retail investors should not merely supply liquidity for Africa’s biggest businesses.

They should receive transparent information, enforceable rights and a fair opportunity to participate in the upside.

Economic Implication

Investor demand is itself a valuable financial asset. Unauthorized marketers were attempting to capture that demand before approved disclosures, pricing and allocation rules existed.

A legitimate IPO could broaden participation in African industrial ownership. But the structure of the offering will determine whether ordinary investors gain meaningful exposure to the refinery’s future earnings or primarily provide capital while control remains concentrated.

Why It Matters

Black economic development requires more than encouraging people to invest.

It requires markets where ordinary investors can verify what they are buying, understand the risks and enforce their ownership rights.

Without those protections, public appetite for African ownership can become a source of liquidity for promoters rather than a path to household wealth.

The Ownership Question

Will retail investors receive transparent, fairly structured access to the refinery’s future earnings—or mainly be used to generate demand around the offering?

Disclosure: This article is independent editorial analysis based on information from Nigeria’s Securities and Exchange Commission and Reuters. It is not investment advice and is not affiliated with Dangote Group, Dangote Petroleum Refinery, Nigeria’s SEC or any brokerage or capital-market operator.

Latest posts by normbond (see all)

- Dangote Refinery Plans $5 Billion IPO That Could Become Africa’s Largest Listing - August 5, 2026

- FIFA Wants to Turn the World Cup Into a $20 Billion Company. Who Owns Global Football After That? - July 29, 2026

- Cape Town Approved a 170-Megawatt Data-Center Project. The Community Still Does Not Know the Full Resource Cost. - July 29, 2026