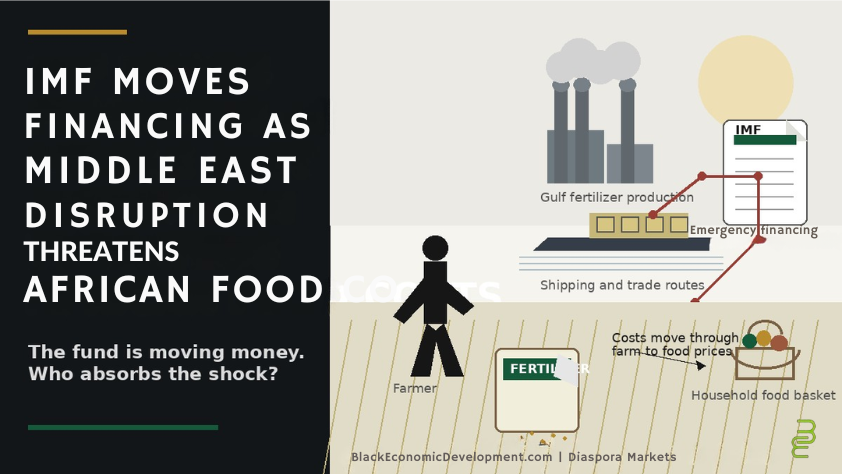

The fund is increasing support for Burkina Faso, The Gambia, São Tomé and Príncipe, and Ethiopia as fertilizer disruptions threaten farm expenses, food prices, foreign-exchange reserves, and government budgets.

A ceasefire may reduce the immediate fighting in the Middle East, but it will not instantly repair the supply chains African food systems depend on.

Zeine Zeidane, the International Monetary Fund’s new African Department director, said fertilizer production and exports from Gulf countries could take six to seven months to return fully to normal.

The IMF has reached staff-level agreements to provide additional financing for Burkina Faso, The Gambia, and São Tomé and Príncipe in response to the conflict’s economic effects. For Ethiopia, the fund has accelerated approximately $200 million within an existing financing program.

The movement of money signals how quickly a conflict outside Africa can become an African food-cost, currency, and sovereign-financing problem.

Emergency liquidity may help governments maintain essential imports and reduce immediate pressure. But the deeper economic question remains:

Who ultimately absorbs the adjustment—governments, farmers, food businesses, lenders, or households?

Why the disruption matters for African food systems

Fertilizer is one of the costs built into food production.

When fertilizer becomes more expensive or difficult to obtain, farmers may have to pay more, use less, switch crops, or reduce the amount of land they plant.

Each option carries consequences.

Higher input expenses can increase the price needed to produce food profitably. Lower fertilizer use can weaken yields. Reduced planting can limit domestic supply.

The pressure then moves through the rest of the food system.

Importers need additional foreign currency to purchase the same quantity of fertilizer. Governments face demands for subsidies or emergency support. Food processors and retailers may pass higher costs to consumers.

Central banks may also face another source of inflation at a time when many countries are already managing limited reserves, currency pressures, and elevated borrowing needs.

In Burkina Faso, the IMF has said sharp increases in international fertilizer and petroleum prices following the Middle East conflict weakened the near-term outlook and created immediate risks for food security and the balance of payments.

In Ethiopia, the fund said the conflict caused sharp price increases for key imports, including fuel and fertilizer.

This is how disruption in a Gulf production facility or shipping route reaches a farmer’s field—and eventually a household food budget—thousands of miles away.

Where the money is moving

The IMF is directing additional liquidity toward governments with limited room to absorb a prolonged external shock.

Burkina Faso has requested an increase in access under its Extended Credit Facility program. The proposed augmentation is intended to respond to a balance-of-payments shock linked to higher fertilizer and petroleum prices.

If approved by the IMF Executive Board, the review and requested increase would enable a new disbursement under the program.

The Gambia and São Tomé and Príncipe have also reached staff-level agreements for increased financing related to the conflict’s effects, according to Zeidane.

Ethiopia already has a four-year, $3.4 billion IMF-supported program. A recent staff-level agreement on its fifth review could make approximately $468 million available after management and board approval. IMF officials also accelerated access to roughly $200 million as the country confronted higher import costs.

This money can help countries pay import bills, support foreign-exchange reserves, and avoid a more abrupt financing crisis.

But the financing does not eliminate the cost of the shock.

It changes when the cost is paid, how it is distributed, and which institutions influence the response.

What IMF financing can—and cannot—do

Emergency financing can provide governments with valuable breathing room.

It can help maintain fertilizer, fuel, and food imports when export income or reserves are insufficient. It can reduce the risk of sudden shortages and give governments more time to organize targeted support.

It may also reassure other creditors and development institutions that a country has a financing framework in place.

But IMF support generally operates through broader economic programs with policy commitments, performance reviews, and repayment obligations.

That does not automatically make the financing harmful. In a severe external shock, failing to secure liquidity could lead to sharper currency losses, import shortages, inflation, or cuts in essential spending.

The question is how the financing is structured and where the protection reaches.

A loan that stabilizes reserves but does not keep fertilizer affordable for farmers may protect the national balance sheet without fully protecting the food system.

A program that helps maintain imports today but contributes to tighter future budget choices may transfer part of the shock to taxpayers and public services later.

The relevant measure is not simply how much money enters the country.

It is who is protected by the financing and who remains exposed.

Who captures the immediate upside?

Governments capture the first layer of relief.

Additional financing can support reserves, pay for essential imports, ease immediate balance-of-payments pressure, and prevent a faster deterioration in public finances.

Large importers and distributors may also benefit when additional foreign currency allows fertilizer, fuel, and other essential goods to continue moving.

The IMF gains a central role in the policy response through its financing relationships. Its programs can influence decisions involving exchange rates, revenue collection, public spending, subsidies, and fiscal management.

The potential benefit for households is less direct.

Families benefit only when the financing helps maintain food availability, contain price increases, protect employment, and preserve essential public services.

That outcome depends on government policy, distribution systems, market behavior, and whether relief reaches farmers and consumers rather than stopping at the level of national accounts.

Who carries the risk?

Farmers carry immediate production risk.

They may need to purchase more expensive fertilizer months before they receive income from a harvest. Small farmers with limited cash or credit are especially vulnerable to that mismatch.

Some may reduce fertilizer use to save money. That choice can lower yields and create a second problem later in the season.

Importers carry foreign-exchange and supply risk. Food processors and retailers face higher operating costs and uncertainty about how much consumers can afford.

Governments face pressure from several directions at once.

They may be asked to subsidize fertilizer, protect fuel prices, support vulnerable households, defend currencies, and preserve public services—all while managing debt and limited fiscal space.

Households often carry the final burden.

When higher costs reach retail markets, families may have to spend more on staple foods while reducing spending on transportation, education, health care, or housing.

Lower-income households are especially exposed because food represents a larger share of their total spending.

Emergency protection or future debt?

The IMF’s intervention raises a difficult but necessary question:

Does emergency financing protect African food systems, or does it move part of the shock into future debt and spending constraints?

The answer can be both.

Financing can prevent an immediate crisis while also adding obligations that shape future budgets.

The outcome depends on the terms of the financing, what governments do with the additional resources, how long the disruption lasts, and whether the borrowing supports stronger productive capacity.

Emergency money is most protective when it helps maintain essential imports, provides targeted assistance to small farmers, strengthens social protection, and prevents temporary shortages from becoming permanent production losses.

It is less transformative when it only fills a foreign-exchange gap without reducing the underlying dependence on imported inputs.

In that case, governments borrow to survive the current disruption but remain vulnerable to the next one.

The ownership question behind the fertilizer shock

Africa’s exposure is not only about geography.

It is also about who owns and controls the fertilizer value chain.

The important assets include fertilizer plants, natural-gas inputs, phosphate resources, shipping routes, ports, storage facilities, trade finance, distribution networks, and the foreign currency needed to make purchases.

African farmers produce the food.

But in many countries, they do not control the essential imported inputs or financing systems required to produce it affordably.

Governments may subsidize fertilizer, but subsidies do not create ownership of production capacity.

Countries may import from global suppliers, but purchasing power is not the same as control over supply.

The central ownership question is:

Who controls the fertilizer production, financing, shipping, storage, and distribution systems that determine whether African farmers can afford to plant?

A second question follows:

When African governments need external financing to protect essential imports, who gains economic and policy leverage by supplying the capital?

Food security requires more than liquidity

IMF support may be necessary during an immediate crisis.

But emergency liquidity is not the same as food sovereignty.

Long-term resilience requires greater African control over fertilizer production, regional procurement, storage, transport infrastructure, agricultural credit, and cross-border trade.

The continent has substantial agricultural demand and many of the raw materials needed for fertilizer production. Yet numerous countries remain dependent on external producers, shipping systems, commodity traders, and lenders.

That dependency allows a conflict elsewhere to raise the cost of planting food across Africa.

Regional purchasing agreements could improve bargaining power.

Strategic fertilizer reserves could provide a buffer when shipments are delayed.

Expanded African production could keep more value inside the continent while reducing exposure to distant supply disruptions.

Better railways, ports, warehouses, and distribution systems could also reduce the domestic costs added after fertilizer reaches African markets.

None of these steps would eliminate international trade.

The goal is not complete self-sufficiency in every input. It is enough production, storage, financing, and regional coordination to prevent every external shock from becoming a food and debt emergency.

What this reveals about African economic power

This disruption shows the difference between having agricultural potential and controlling the systems that turn that potential into affordable food.

Africa has farmers, land, labor, growing markets, and natural resources.

But much of the leverage still sits with external fertilizer producers, shipping companies, commodity traders, foreign-currency markets, and international lenders.

That structure determines who sets prices, who receives payment first, who earns returns from financing, and who absorbs losses when the system is disrupted.

African governments can reduce that vulnerability by treating fertilizer and agricultural infrastructure as strategic economic assets rather than routine imports.

That means investing not only in farms, but in the entire chain that supports them.

It also means asking whether emergency borrowing is being used simply to restore the old dependency—or to build a more resilient system.

Why it matters

The Middle East disruption demonstrates how quickly geopolitics can move into African kitchens.

A delayed fertilizer shipment can become a higher farm expense.

A higher farm expense can become reduced planting or a more expensive harvest.

That can become food inflation, pressure on household budgets, and another demand on governments already managing debt and limited foreign exchange.

The IMF can provide liquidity and reduce immediate instability.

It cannot manufacture fertilizer inside African economies, build regional storage systems, expand farmer credit, or guarantee that financial relief reaches households.

That requires public policy, regional coordination, productive investment, and ownership of more of the agricultural value chain.

The immediate financing may help prevent a sharper crisis.

The longer-term test is whether African countries emerge with stronger food systems—or with larger obligations and the same vulnerability before the next disruption.

Latest posts by normbond (see all)

- FIFA Wants to Turn the World Cup Into a $20 Billion Company. Who Owns Global Football After That? - July 29, 2026

- Cape Town Approved a 170-Megawatt Data-Center Project. The Community Still Does Not Know the Full Resource Cost. - July 29, 2026

- LeBron Took an $8 Million Deal. The 76ers May Capture the Bigger Economic Win. - July 24, 2026