The racial wealth gap is often discussed as if it is mainly about wages, education or personal savings.

Those things matter.

But they do not fully explain why the Black-white wealth gap has lasted for more than 150 years after Emancipation.

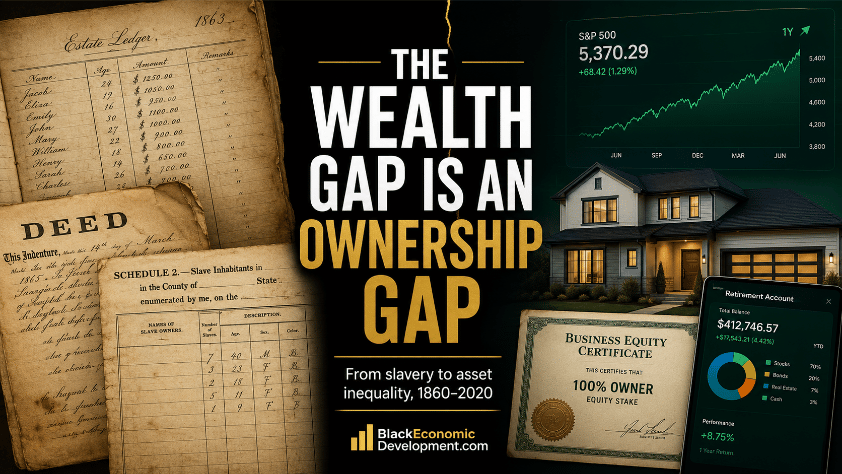

A major study published in The Quarterly Journal of Economics offers a deeper explanation: the gap is rooted in ownership. The paper, “Wealth of Two Nations: The U.S. Racial Wealth Gap, 1860–2020,” constructs a long-run record of the white-to-Black per capita wealth ratio from 1860 to 2020 and finds that the racial wealth gap remains one of the largest and most persistent economic disparities in the United States.

That matters because wealth is not just money in a bank account.

- Wealth is home equity.

- Business ownership.

- Stocks.

- Retirement accounts.

- Land.

- Inheritance.

- Intellectual property.

- Access to credit.

- The ability to survive a crisis without losing everything.

Income helps a household live.

Wealth helps a household move.

The Gap Started With Different Starting Lines

The study’s most important point is also the one America often tries to skip.

Black Americans did not enter freedom with the same asset base as white Americans.

After slavery, Black families were forced to build from dramatically different starting conditions. The paper argues that even if Black and white Americans had faced equal wealth-building conditions after Emancipation, full convergence would still have remained distant because the initial wealth divide was so large.

That changes the question.

The question is not simply, “Why did Black families not save more?”

The better question is:

What assets were Black families allowed to own, protect, grow, borrow against, and pass down?

That is the ownership question.

And once ownership becomes the lens, the racial wealth gap looks less like a mystery and more like a system doing what it was built to do.

Why Income Alone Cannot Close the Gap

Wages matter. Jobs matter. Education matters.

But income is not the same as wealth.

A household can earn more money and still struggle to build wealth if most of that income is absorbed by housing costs, debt payments, health expenses, family support, inflation or emergencies.

A household with wealth has more options.

- It can buy a home before prices rise.

- It can invest when markets fall.

- It can start a business.

- It can help a child avoid debt.

- It can move for opportunity.

- It can wait out a downturn.

That is the difference between earning income and owning assets.

The modern economy rewards ownership heavily. Homes appreciate. Stocks rise. Business equity compounds. Retirement accounts grow. Inheritances transfer advantages across generations.

When Black households are less likely to hold those assets at scale, they can work hard and still fall behind in the wealth race.

That is why the racial wealth gap is not only a labor-market issue.

It is a capital-market issue.

The Gap Stalled After 1950

The Quarterly Journal of Economics study finds that racial wealth convergence slowed over the past 150 years and stalled after 1950. Since the 1980s, the gap widened again as capital gains mostly benefited white households, while convergence through income growth and savings came to a halt.

That is the modern story.

The gap is not frozen only because of the past.

It is reproduced by the present.

When the economy rewards people who already own assets, those with the largest starting positions capture more of the upside.

This is especially important in a period when the stock market, housing market, retirement system, private equity, technology platforms, and business ownership are central to wealth creation.

The upside flows to ownership.

The risk flows to those without enough assets to absorb volatility.

Black Wealth Has Risen, But the Gap Remains Large

Recent data shows how complicated progress can be.

According to Federal Reserve Survey of Consumer Finances data discussed by the Brookings Institution, median Black wealth rose from $27,970 in 2019 to $44,890 in 2022. That is real growth. But median white wealth was still about $285,000 in 2022.

That means Black wealth can rise and the racial wealth gap can still remain structurally large.

This is the part that often gets missed.

Percentage gains do not automatically close dollar gaps.

When one group starts with far more assets, even modest asset growth can increase the absolute distance between groups.

A family with $300,000 in assets that gains 10 percent adds $30,000.

A family with $30,000 in assets that gains 20 percent adds $6,000.

- The second family had the higher percentage gain.

- The first family captured more dollars.

That is how compounding works.

And compounding is one of the quiet engines of racial wealth inequality.

Who Captures the Upside?

This is where the economics becomes clear.

In an asset-driven economy, the biggest gains often go to households that already own appreciating assets.

- That includes homeowners in rising markets.

- Investors with large portfolios.

- Business owners with equity.

- Families receiving inheritances.

- Workers with retirement accounts tied to market gains.

- People with enough savings to buy when asset prices are low.

The core issue is not whether Black Americans are working.

The issue is whether Black Americans are positioned to own what appreciates.

That includes homes, businesses, land, stocks, retirement assets, intellectual property, media platforms, data, and equity in high-growth industries.

- Black labor creates value.

- Black culture creates value.

- Black consumers create value.

- Black creators create value.

- Black entrepreneurs create value.

But the wealth question is about who owns the asset that captures that value after the transaction is over.

The Policy Question Is Also an Ownership Question

If the racial wealth gap is an ownership gap, then the solutions must go beyond income.

Better jobs help.

Higher wages help.

Financial literacy helps.

But they are not enough by themselves.

The ownership gap points toward a broader set of policy and market questions:

- Who gets access to affordable homeownership?

- Who gets business capital?

- Who benefits from public procurement?

- Who receives inheritances?

- Who has access to retirement plans?

- Who gets fair appraisals?

- Who owns land?

- Who gets equity, not just wages?

- Who has protection against predatory debt?

- Who owns the platforms where Black culture becomes revenue?

This is why wealth-gap policy cannot only focus on individual behavior.

- Budgeting matters.

- Saving matters.

- Investing matters.

But the gap was not created by individual choices alone.

It will not be closed by individual choices alone.

Why This Matters Now

This conversation is urgent because the U.S. economy is becoming even more asset-driven.

Artificial intelligence is creating new productivity gains, but platform owners may capture much of the value.

Real estate remains a major path to household wealth, but affordability is moving out of reach for many first-time buyers.

Creator platforms monetize Black attention, but platform companies often control the data, distribution and advertising infrastructure.

Sports, entertainment, and media generate massive Black cultural value, but ownership of teams, catalogs, networks, studios and platforms remains limited.

The lesson is consistent.

- Participation is not the same as ownership.

- Visibility is not the same as control.

- Income is not the same as wealth.

The Economic Implication

The racial wealth gap is best understood as a long-running ownership gap.

- It began with unequal starting points after slavery.

- It was reinforced by exclusion from land, credit, housing, capital markets and wealth-building institutions.

- It continues today because the modern economy rewards existing asset ownership.

The question is not only how much Black households earn.

The question is what Black households own, what those assets are worth, and whether those assets can compound across generations.

Why It Matters

For Black communities, this reframes the wealth conversation.

The goal cannot only be better paychecks.

The goal must include stronger ownership positions.

That means homeownership, business ownership, retirement participation, stock ownership, land retention, estate planning, fair lending, procurement access, intellectual property control and equity in emerging industries.

It also means protecting Black communities from losing assets through displacement, heirs’ property loss, predatory lending, business undercapitalization and market exclusion.

The racial wealth gap is not just a number.

It is a map of who has been able to turn time into capital.

And the future of Black economic development depends on whether Black communities can own more of what grows.

Latest posts by normbond (see all)

- FIFA Wants to Turn the World Cup Into a $20 Billion Company. Who Owns Global Football After That? - July 29, 2026

- Cape Town Approved a 170-Megawatt Data-Center Project. The Community Still Does Not Know the Full Resource Cost. - July 29, 2026

- LeBron Took an $8 Million Deal. The 76ers May Capture the Bigger Economic Win. - July 24, 2026