The acquittal of a South Carolina convenience-store owner in the killing of 14-year-old Cyrus Carmack-Belton has renewed a difficult conversation about neighborhood commerce, community accountability and who captures the wealth created by Black consumer spending.

Five years ago, I posted a simple question after spending several weeks in North Philadelphia:

What happened to the Black-owned corner stores?

I remembered a time when Black entrepreneurs owned more of the small stores serving Black neighborhoods. But during that visit, I could not identify a single Black-owned corner store in the area around me.

The Facebook discussion that followed offered no easy answer.

Some people blamed inadequate customer support. Others pointed to bank financing, crime, estate planning, government licensing, gentrification, competition from national chains and the failure to transfer family businesses to the next generation.

Those comments were opinions, not a formal economic study. But together, they revealed an important truth:

The disappearance of Black-owned neighborhood retail cannot be explained by one slogan or one group of people.

It is the result of multiple pressures involving ownership, capital, property, succession, consumer behavior and public policy.

Now, a verdict in South Carolina has made the original question feel even more urgent.

The case that brought the issue back into focus

On June 1, 2026, a South Carolina jury found 61-year-old convenience-store owner Chikei Rick Chow not guilty of murder in the 2023 shooting death of 14-year-old Cyrus Carmack-Belton.

The encounter began after Chow suspected Carmack-Belton of stealing four bottles of water from his Columbia-area convenience store. Prosecutors said the teenager returned the bottles and left the store before Chow and his son pursued him for more than 130 yards.

Chow then shot Carmack-Belton in the back.

Prosecutors acknowledged that Carmack-Belton had been carrying a semiautomatic pistol, but they argued that it fell during the chase and that he never threatened Chow or his son with it. The defense maintained that the teenager pointed the weapon at Chow’s son and that Chow fired to protect him.

The jury acquitted Chow after hearing those competing accounts. Carmack-Belton’s family has said it plans to continue pursuing a civil lawsuit.

The criminal verdict answered whether prosecutors proved the murder charge beyond a reasonable doubt.

It did not answer the larger questions surrounding neighborhood commerce, merchant power and community trust.

A corner store is more than a place to buy groceries

A neighborhood convenience store may look like a small operation, but it sits at the intersection of several valuable economic systems.

The owner controls access to food, household necessities, lottery sales, tobacco products, financial services and, in some locations, fuel.

- The business generates cash flow.

- The building may generate rent and property appreciation.

- Wholesalers earn money supplying the inventory.

- Banks and payment processors collect fees.

- Insurance companies, delivery platforms, franchisors and fuel distributors may also receive a share of every dollar moving through the location.

The store owner controls more than merchandise. The owner also controls an important neighborhood relationship.

That includes decisions about hiring, security, surveillance, customer treatment, informal credit and when law enforcement becomes involved.

In communities with few supermarkets or full-service retailers, residents may have limited alternatives. A privately owned store can therefore function as part of the neighborhood’s essential infrastructure.

That makes the ownership question economically significant.

Who captures the money spent in Black neighborhoods?

Black consumers may provide much of the revenue flowing through neighborhood stores without owning a proportional share of the businesses, buildings or supply relationships behind them.

- Residents receive products and convenience.

- Employees may receive wages.

- But the long-term upside generally belongs to those who own the assets.

- The business owner captures the operating profit.

- The property owner captures rent and appreciation.

- The distributor captures wholesale revenue.

- The lender collects interest.

And when the store or building is sold, the owner receives the value created through years of neighborhood spending.

This is not an argument that immigrant or non-Black entrepreneurs should not operate businesses in Black communities.

Entrepreneurs frequently enter markets where they recognize demand and are willing to accept the risks.

The economic question is different:

Why are Black residents so often the primary customer base without holding a comparable ownership stake in the commercial assets serving that base?

What happened to Black-owned neighborhood retail?

There is no single explanation.

Many small retailers operate on thin margins. They face rising inventory costs, theft, insurance expenses, security concerns, equipment failures and competition from dollar stores, supermarkets, delivery services and online retailers.

Access to capital also matters.

A business owner who cannot obtain affordable financing may struggle to replace refrigeration, renovate a property, purchase inventory in volume or survive a temporary drop in sales.

Property ownership matters too.

An entrepreneur who owns the building can accumulate equity and exercise greater control over operating costs. A tenant remains vulnerable to rent increases, redevelopment and displacement.

Succession is another major issue.

A profitable store can still disappear when an owner retires or dies without a clear transfer plan. Without estate planning, management training or interested heirs, a family business may be sold rather than passed to the next generation.

The original Facebook discussion also raised the role of customer behavior. Community support can influence whether a local store survives.

But “Black people do not support Black businesses” is not a sufficient economic analysis.

Philadelphia provides evidence of a more complicated business landscape. Pew reported that the number of Black-owned employer businesses in the city increased from about 1,150 in 2012 to 1,990 in 2022.

Even with that growth, those firms represented only 9.2% of Philadelphia’s employer businesses whose ownership could be classified by race, ethnicity or sex.

The problem is not simply a lack of entrepreneurial interest.

It is also a question of business scale, financing, commercial property and the ability to remain open long enough to build transferable wealth.

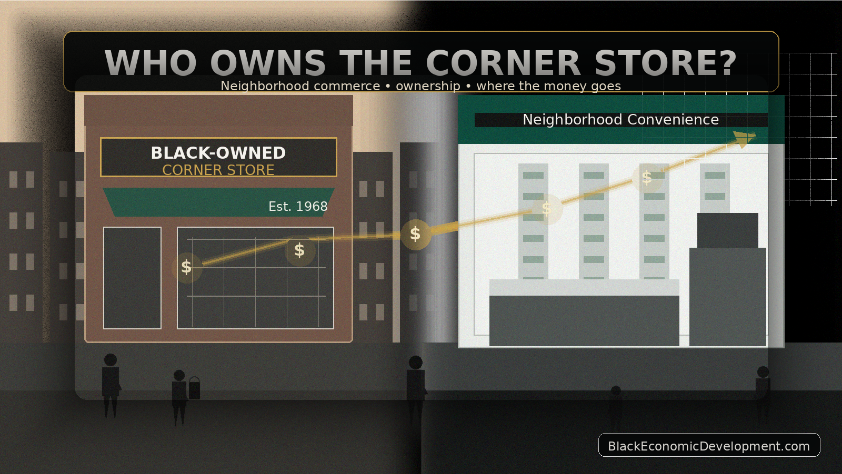

North Philadelphia already has an ownership model worth studying

North Philadelphia is home to one of the most important examples of Black commercial ownership in the country.

Founded in 1968 by the Rev. Leon H. Sullivan, Sullivan Progress Plaza became the first shopping center in the United States developed, owned and managed by African Americans.

The project was financed with support from Zion Baptist Church members, local Black residents and individual investors. It demonstrated that a community could pool capital, develop commercial property and negotiate with major retailers from an ownership position.

That model went beyond telling people where to shop.

It addressed who owned the land, who controlled the development and who benefited from the value created there.

That distinction remains central to Black economic development.

Consumer loyalty can help a business survive. But ownership of commercial real estate and distribution systems creates another level of economic power.

Who carries the risk?

When neighborhood commerce breaks down, the risks are not distributed equally.

Store owners face robbery, theft, property damage, financial loss and physical danger.

Employees may face those same dangers without receiving any ownership stake.

Residents carry the risk of poor service, limited food access, aggressive surveillance and conflicts with merchants who may not feel accountable to the surrounding community.

Families carry the deepest cost when a commercial dispute turns deadly.

The confrontation involving Carmack-Belton began with a suspicion involving four bottles of water. It ended with a teenager dead, a merchant prosecuted, a store vandalized, years of legal proceedings and a community left with grief and anger.

There was no meaningful economic winner.

Black ownership is necessary, but it is not enough

Increasing Black ownership would not automatically eliminate conflict, mistreatment or violence.

Black-owned businesses must also be professionally operated and accountable to the communities they serve.

That means strong customer-service standards, responsible security policies, conflict-management training and clear rules against armed pursuit over suspected shoplifting.

It also means recognizing that ownership is not simply about the identity of the person behind the counter.

The real economic-development goal is to build institutions that create local employment, retain community spending, preserve commercial property and operate with dignity and accountability.

A Black-owned store that exploits workers or mistreats customers is not an economic-development success.

At the same time, a neighborhood that generates millions of dollars in recurring consumer demand but owns few of the businesses or properties receiving that money has limited economic leverage.

Both realities can be true.

What rebuilding Black neighborhood retail would require

The answer cannot be reduced to “buy Black.”

Consumer support is important, but entrepreneurs also need the infrastructure required to compete.

That includes affordable capital, business training, cooperative purchasing, commercial-property acquisition and reliable access to distributors.

It requires estate planning and succession strategies so stores can become multigenerational assets rather than businesses that disappear when the founder retires.

It may also require community investment funds, credit-union partnerships and shared service organizations that help independent retailers manage accounting, technology, insurance and security.

Public policy has a role as well.

Cities can examine whether licensing, zoning, procurement, grants and commercial lending programs are helping neighborhood residents acquire ownership or merely attracting outside operators into underserved markets.

The goal should not be to remove one ethnic group and replace it with another.

The goal should be to expand Black participation in the ownership, financing and governance of the businesses serving Black communities.

The question is bigger now

Five years ago, I asked what happened to the Black-owned corner stores.

Today, the better question may be:

What would it take to build a new generation of neighborhood businesses that are locally owned, adequately financed, professionally operated and accountable to the communities whose spending keeps them alive?

The corner store is not only where money is spent.

It is where relationships are formed, risks are negotiated and economic value is created.

The community should have a meaningful stake in all three.

Economic Implication

Everyday neighborhood spending creates business revenue, rental income, property appreciation and transferable wealth. When Black communities do not own the stores, buildings or distribution networks serving them, less of that economic value remains under local control.

Why It Matters

The Chow case is primarily a story about the loss of a young life and a contested claim of defense of another person. It also exposes the fragile relationship that can develop when merchants hold commercial power inside communities where residents have limited retail ownership or influence.

The challenge is not simply opening more stores.

It is building a retail ecosystem in which Black communities participate as owners, investors, workers, suppliers and decision-makers.

Over to You

What is the ownership question in your neighborhood? Who owns the stores, the buildings and the supply systems receiving the community’s everyday spending?

Latest posts by normbond (see all)

- LeBron Took an $8 Million Deal. The 76ers May Capture the Bigger Economic Win. - July 24, 2026

- Lina Khan Is Entering New York City’s Development Machine. Who Gets the Land, Contracts, and Upside? - July 22, 2026

- If Workplace Race Data Disappears, Discrimination Becomes Harder to See—and Harder to Prove - July 22, 2026